About a Woods in North Central Indiana

Thirty seven growing seasons ago in January of 1980, at 31 years of age, I purchased a 16-acre parcel which included a 4-acre cornfield and 12 acres of woods. My primary purpose was a long-term timber production investment. I also decided to track the growth of the timber and cost and income from sales, so that someday I could write such an article as this. I paid $1,150 per acre for 16 acres. I planted the 4-acre cornfield to trees in the spring of 1981. Of the remaining 12 acres, 1.5 acres was a stand of young elm. I sold the elm as firewood and planted black walnut. These 5.5 acres of tree plantings are doing very well and would be a good topic for a future article; however, this article is about the productivity of the remaining 10.5 acres of woodland.

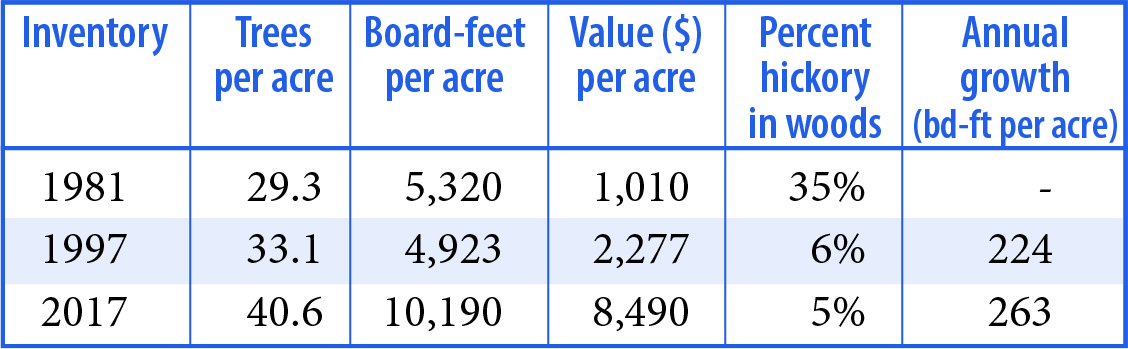

This woodland is located on rolling glacial till sandy loam soils making this a little better than an average timber producing site for northern Indiana. This woods has a small stream that has water flow only during wet periods. There is a log yarding area of about one-half acre within the woods and next to the county road. Previous owners had high-grade harvested the woods and had periodically grazed livestock in the woods. This resulted in the overstory being dominated by hickory and low quality oak. Hickory is a slow growing and lower value species making it a poor tree to have as your main species in a timber investment woodland. The younger trees were much more encouraging and were the main reason I bought the property. These younger trees were mostly 8 to 12 inches diameter at breast height (DBH), and included many quality black walnut and black cherry. My 100% inventory of all merchantable trees 12 inches DBH and larger showed there to be 5,320 board feet per acre Doyle scale at the time of purchase. I appraised the 1981 beginning volume to have a stumpage timber value of $1,010 per acre. The beginning volume included 13 species of which 35% was hickory. This woodland was producing well below its potential because of a poor species mix, low timber quality, and a less than ideal stocking level among over story trees.

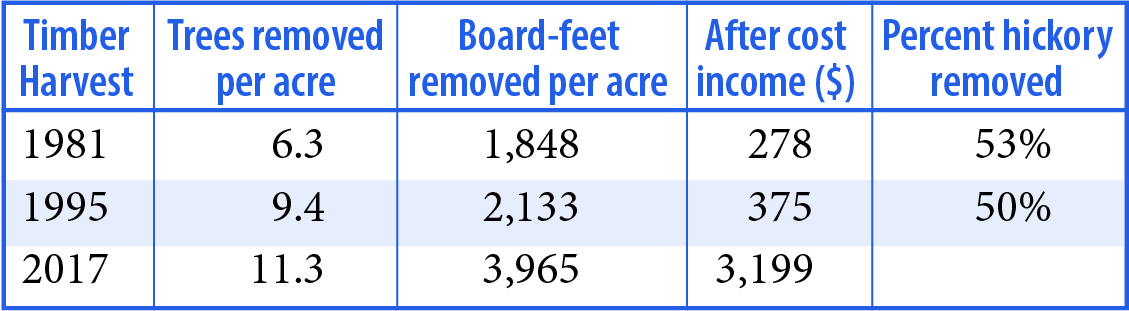

My first step in the management of this woods was to have an improvement type timber sale in 1981. This sale included 66 trees, having 19,404 bd.ft., 35 hickory, and over mature and defective oak. After the harvest, I did timber stand improvement (TSI) work to complete the harvest openings, to kill cull trees, to cut grape vines, and to do some crop tree release among the pole sized trees. The income from the sale after deducting consulting forester timber sale and TSI cost was $2,919 or $278/acre.

I conducted my second timber sale in 1995. This was also an improvement type harvest including 99 trees, having 22,396 bd.ft. Doyle. Fifty of these trees were hickory, and the other 49 were again mostly lower quality oak trees. I again did TSI after the harvest completing regeneration openings and doing crop tree release. The income from this sale after consulting forester TSI and sale costs were deducted was $3,934 or $375/acre.

After this second harvest was completed, in 1997 I did my second 100% inventory of the merchantable timber and found 4,923 bd.ft./acre having a value of $2,277/acre. The beginning 1980 volume had been 5,320 bd.ft./acre with a value of $1,010/acre. That worked out to a growth rate of 224 board feet per acre per year, which is a volume growth rate of 3.5% per year. The value per acre was $2,277/acre or 2.25 times greater than the beginning value. After 16 growing seasons and two timber harvests I was just 400 bd.ft. per acre below my beginning timber volume, but my timber quality, species mix, and timber value were now much better.

In 2017 I did my third 100% inventory of all merchantable trees. It had been 20 growing seasons since the last inventory with no timber harvested in between. The timber volume went from 4,923 bd.ft. per acre in 1997 to 10,190 bd.ft. per acre in 2017. That works out to 263 bd.ft. per acre per year, for an improvement of nearly 40 bd.ft./ac/yr. from what it was during the first 16 years of my ownership. The species mix had gone from 35% hickory in 1980 to 6% hickory in 2017. Black Cherry (23%), White Oak (21%), Black Walnut (16%), Red Oak (10%), and Burr Oak (10%) were now the main species. My appraisal of the timber value went from $1,010 per acre in 1980 to $8,490 per acre in 2017, and that is after $754 per acre had been sold in the two timber sales. Considering 2017 timber values, and the current tree species and timber quality in this woods, the current growth rate of 263 bd.ft. per acre per year works out to $219 per acre per year of timber growth.

After the 2017 inventory, I conducted my third timber sale. I sold 119 trees having 41,640 bd.ft. The main species in this sale were white oak, black cherry, red oak, burr oak and walnut. Trees were selected based mostly on economic and biologic maturity, and with the idea that the next sale would be in 10 years. I would call this a fairly high-quality sale, which included 3 white oak and 3 black walnut that I estimated to have veneer quality. After deducting the consulting forester sale costs, the income was $33,590, or $0.80/bd.ft. That is a long way from the 1981 sale that got $0.16/bd.ft. That is an increase of 5 times the value per bd.ft. received because of increases in timber prices over time, and an improvement of the species mix and timber quality sold. This is strong evidence that good timber management pays.

This woods has been a good investment. If you factor out the land value and just consider the timber values, my 1980 to 2017 investment has earned an annual compound interest rate of seven percent per year, which I think is quite good. I also think this case study makes a strong statement for the value of good timber management because a 35% stand of hickory and defective oak would not have come close to these earnings.

Bruce Wakeland ACF, CF has 45 years of professional experience as a forester in Indiana. He currently owns and operates Wakeland Forestry Consultants.